Whenever Lotto reaches numbers as large as $55 million, the first thought everyone has is simple: “That’ll last forever.”

But when we start looking at the numbers properly, factoring in returns, inflation, fees, tax, and withdrawals – the picture becomes a lot more interesting. Even life-changing money still needs a plan.

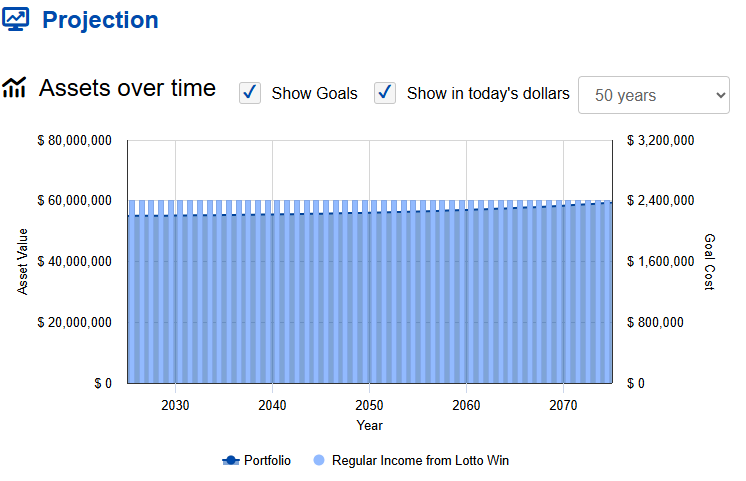

Let’s walk through what a $55 million windfall could actually provide in terms of long-term income. For this exercise we’ll ignore the effect of volatility (however another key component of funding income from portfolios).

Starting Point: Using the FMA’s Long-Run Return (4.5% after tax and fees)

To keep things realistic, imagine the full $55 million is invested in a growth portfolio. Mostly growth assets with a smaller allocation to defensive assets.

Using the FMA’s long-term expected return of 4.5% after tax and fees, a portfolio could comfortably support withdrawals of around $200,000 every month without ever running out of money. In other words, as the average annualised return is higher, you could spend $200,000 a month and still preserve the capital for generations to come.

But When We Add Inflation, the Story Changes

Inflation doesn’t feel like much year to year, but over decades it’s the single biggest force eroding purchasing power. If we use the Reserve Bank’s midpoint inflation rate of 2%, and if your spending increases each year to keep up with rising prices, the maths shifts.

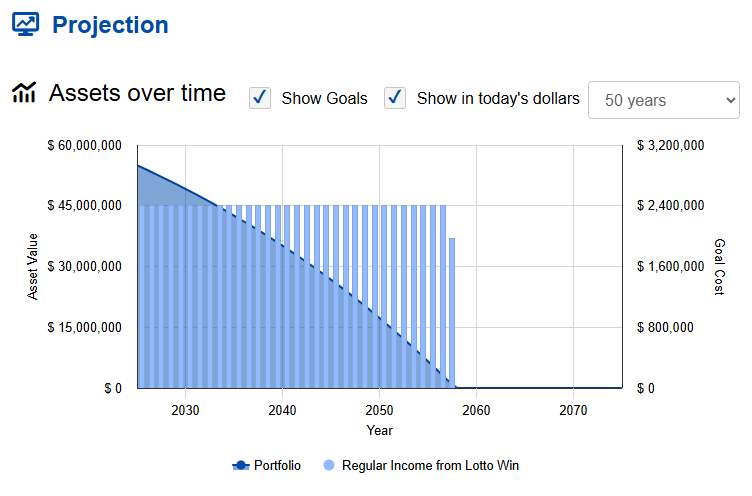

At that same $200,000 per month, but now with increasing your withdrawals every year – your $55 million would last around 32 years. Still extraordinary, but no longer “forever”.

So how do we keep the portfolio in tact?

Many people with significant wealth want two things: stable income and the confidence that the capital will last for generations. When we try to balance both, we need to dial the spending back.

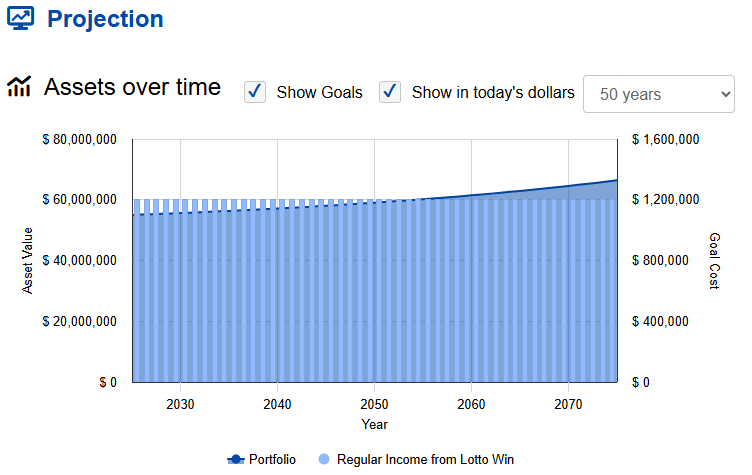

At a 4.5% return after tax and fees, an inflation-protected income that lasts indefinitely looks more like $100,000 per month. This is the level where the portfolio can fund your spending, keep pace with inflation, and still maintain the original capital.

What If Returns Are Higher?

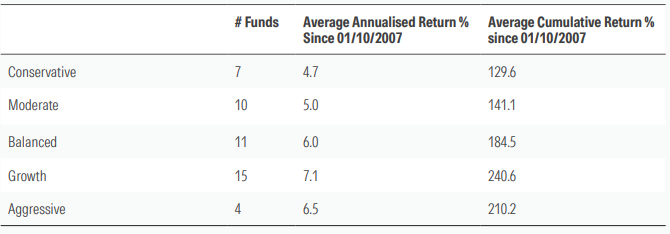

Looking back to the start of KiwiSaver in 2007, the average Growth fund has returned 7.1% per year after fees. To keep things simple, if we assume a 5.5% return after tax and fees, the sustainable income increases meaningfully.

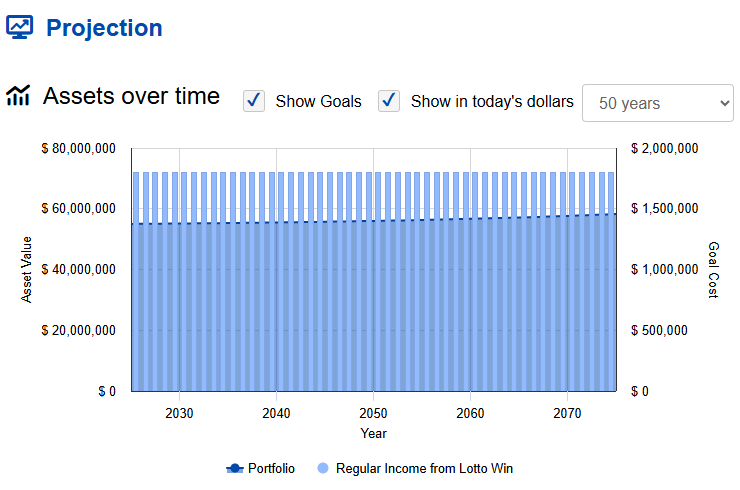

At 5.5%, a long-term, inflation-protected income of around $150,000 per month becomes achievable. So for only 1% increase in return, you increase your income by 50%!

However, if $150,000 p/m is not enough and you want that $200,000 p/m back

Finally, if you want an inflation-protected income of $200,000 per month that lasts indefinitely, the numbers point to a required return of roughly 6.7% after tax and fees. Achievable? Possibly depending on the strategy, diversification, and risk tolerance.

So What’s the Big Takeaway?

A $55 million Lotto win is absolutely life-changing. But even with that amount of money, the outcomes vary hugely depending on how you manage all the different inputs.

Inflation, returns, fees, tax, and your actual spending habits will determine whether your money lasts 10 years, 30 years, or multiple generations.

It’s not about how big the number is on day one it’s about the strategy that follows. If your numbers come up tonight, congratulations in advance – and when the dust settles, I’d be happy to help you turn luck into lasting wealth.

Disclaimer

This blog is for general information only and does not constitute personalised financial advice. Projections are based on assumptions that may change. Past performance is not a guarantee of future results. Please seek personalised advice before making financial decisions.